Here's the weather that affects the natural gas market. Cold causes an increase in residential heating. Hot causes an increase in residential cooling.

Sunday Weather:

https://www.marketforum.com/forum/topic/27234/

Monday Weather:

https://www.marketforum.com/forum/topic/27286/

Tuesday Weather:

https://www.marketforum.com/forum/topic/27371/

Wednesday Weather:

https://www.marketforum.com/forum/topic/27451/

Thursday Weather:

https://www.marketforum.com/forum/topic/27535/

Friday Weather:

https://www.marketforum.com/forum/topic/27627/

Saturday Weather:

https://www.marketforum.com/forum/topic/27672/

Sunday Weather:

https://www.marketforum.com/forum/topic/27756/

Previous natural gas discussions/threads

:

Previous discussions on natural gas here:

https://www.marketforum.com/forum/topic/26861/

https://www.marketforum.com/forum/topic/26506/

https://www.marketforum.com/forum/topic/26105/

https://www.marketforum.com/forum/topic/25678/

https://www.marketforum.com/forum/topic/25189/

https://www.marketforum.com/forum/topic/24662/

https://www.marketforum.com/forum/topic/24111/

https://www.marketforum.com/forum/topic/23680/

Natural Gas Intelligence from early Monday Morning:

"Natural Gas Futures Near Even Early; Weekend Guidance Trends Warmer"

metmike: Natural Gas modestly to strongly higher this morning despite warmer guidance. Probably just seasonals, low price and low storage as well as good support at last weeks lows and technical bouncing around.

Weather is just now powerful enough right now to make much difference in demand/usage.

Look how fast the mild weather in December and early January caused us to close the storage gap below. But the gap widened some vs the 5 year average and last year again because of extreme cold several weeks ago.

We turned very chilly late last March into April(2018) with some unusually late season drawdowns............so the current deficit from last year has started to erode.

Note: The shaded area indicates the range between the historical minimum and maximum values for the weekly series from 2014 through 2018. The dashed vertical lines indicate current and year-ago weekly periods.

Last Thursday's EIA report was a bearish surprise!

Led by South Central, EIA Report Shows Massive First Storage Injection

11:20 AM

The Energy Information Administration reported a 23 Bcf injection into storage inventories for the week ending March 29, massively larger.

Closing comments: Large Storage Build Sends Natural Gas Futures Lower

+23 bcf

| Historical Comparisons | |||||||||||||||||||||||||

| Stocks billion cubic feet (Bcf) | Year ago (03/29/18) | 5-year average (2014-18) | |||||||||||||||||||||||

| Region | 03/29/19 | 03/22/19 | net change | implied flow | Bcf | % change | Bcf | % change | |||||||||||||||||

| East | 210 | 225 | -15 | -15 | 231 | -9.1 | 271 | -22.5 | |||||||||||||||||

| Midwest | 241 | 248 | -7 | -7 | 269 | -10.4 | 339 | -28.9 | |||||||||||||||||

| Mountain | 64 | 62 | 2 | 2 | 87 | -26.4 | 115 | -44.3 | |||||||||||||||||

| Pacific | 113 | 104 | 9 | 9 | 166 | -31.9 | 203 | -44.3 | |||||||||||||||||

| South Central | 502 | 467 | 35 | 35 | 606 | -17.2 | 705 | -28.8 | |||||||||||||||||

| Salt | 156 | 137 | 19 | 19 | 187 | -16.6 | 199 | -21.6 | |||||||||||||||||

| Nonsalt | 347 | 329 | 18 | 18 | 419 | -17.2 | 506 | -31.4 | |||||||||||||||||

| Total | 1,130 | 1,107 | 23 | 23 | 1,358 | -16.8 | 1,635 | -30.9 | |||||||||||||||||

These were the 7 day temps, ending the last Friday in March that went into last Thursday's EIA number released at 9:30am Central.

These were the (colder) temperatures for the 7 day period ending last Friday............which will go into this Thursday's EIA report.

The point of showing it is to show that natural gas has a strong historical tendency to go up from mid February into April.

The lows in Feb., would be perfectly timed with a typical, end of Winter low, which is followed by increasing prices over 80% of the time into early Spring.

One should also note that at this time of year, when most of the heating season is over, weather/cold temperatures that increases heating demand in the high population centers has less power to determine prices.............as long as supplies aren't precariously low(they are low but not extremely low) or the demand/supply fundamentals are not extremely tight. Fundamentals are actually pretty bearish........note the price is still fairly low even though storage is still less than the 5 year average.....because the market feels very comfortable...... is projecting additional storage gains from supplies gushing in.

Last Thursday's EIA report was a bearish surprise.  Seasonal Chart")

These natural gas price charts aren't the greatest but they do show a likely seasonal bottom.

The Feb price dropped down and tested the Jan lows for the May contract which is now the front month and reversed higher.

Huge support in that zone on the yearly chart, with numerous trips down to between around 2.5 to 2.6 that solidly held.

After the spike higher from the record cold, natural gas has been struggling. Is the top in and we go against strong positive seasonal price action because of supplies hitting the market and expectations of a growing surplus later this year pressuring the price? Or will seasonal strength help to support the market?

NG 7 days

Natural gas 3 months below

Natural gas 1 year chart

Per Dow Jones newswires this morning:

"--Natural-gas prices were higher Monday morning as forecasts for colder

weather in highly-populated regions may spark an uptick in gas demand."

It appears Mike agrees with me that this is not the reason NG prices are higher being that forecasts and models were a good bit warmer vs the Friday runs for the key two week period. So, they're clearly reaching as wx isn't always the primary market moving factor.

Thanks Larry!

Maybe they are looking at the cold snap late this week? This seems like a stretch since it's not sustained and as you said the overall forecast late Friday, especially on the EURO ensembles had more HDD's.

This last 12z operational GFS that just came out is a bit colder but we'll see what the ensembles show.

The 2nd week of April is just not a good time to be hanging your hat/position on individual model solutions though we both agreed, the colder Euro ensembles on Friday afternoon gas ng a late pop.

Natural gas storage reports compared to expections...........last 5 reports, with the estimate for this next one being +10 bcf vs last weeks +23 bcf.

https://www.investing.com/economic-calendar/natural-gas-storage-386

| Release Date | Time | Actual | Forecast | Previous | |

|---|---|---|---|---|---|

| Apr 11, 2019 | 10:30 | 10B | 23B | ||

| Apr 04, 2019 | 10:30 | 23B | 10B | -36B | |

| Mar 28, 2019 | 10:30 | -36B | -40B | -47B | |

| Mar 21, 2019 | 10:30 | -47B | -48B | -204B | |

| Mar 14, 2019 | 10:30 | -204B | -208B | -149B | |

| Mar 07, 2019 | 11:30 | -149B | -141B | -166B |

Mike said; "Maybe they are looking at the cold snap late this week? This seems like a stretch since it's not sustained and as you said the overall forecast late Friday, especially on the EURO ensembles had more HDD's."

---------------------------------------------------------------------------------------------------

Yes they are per DJ:

"'Cooler conditions will spread across the northern and central U.S.

Wednesday through Sunday with lows of 20s and 30s for stronger national

demand,' said NatGasWeather.com in a statement Monday. 'Cooling will attempt to

reach the east next weekend.'"

However, the problem with that logic is that at same "cold" snap looks significantly less cold than it looked as of the 12Z Fri models:

1. The 0Z Monday EPS is a whopping 23 HDD warmer than that colder 12Z Fri EPS that moved the market over a penny late. This is mainly due to big HDD losses for 4/11-19, which encompass that cold snap. That colder 12Z Fri EPS had been a whopping 17 HDD colder than the 0Z Fri EPS. Therefore, the 0Z Mon EPS is actually 6 HDD warmer than the 0Z Fri EPS!

2. The 0Z Monday GEFS is 13 HDD warmer than the 12Z Fri GEFS, mainly due to a significantly warmer 4/12-17.

3. The morning forecast for Radiant was ~9 HDD warmer than their Fri morning forecast.

Conclusion: I don't see how changes in wx forecasts/models could have possibly lead to higher NG prices this morning. It had to be due to other factors.

Last year during this time frame was near record chilly for the Midwest/East natural gas high population centers.

As noted above, this year, we already had our first injection of natural gas +23 bcf.....compared to last year(2018) when there was a withdrawal -34 bcf for the same week.

For the next 4 weeks, this is what I have for the 2018 EIA reports.

-20 bcf

-34 bcf

-20 bcf

+60 bcf

Last weeks +23 bcf was compared to last years -34 bcf.

So we didn't have our first injection last year until the END of April.

As a result, we should be closing some of the storage deficit gap with 2018 over the next 3 weeks, at a time when, last year, there was a total drawdown of -74 bcf, which has got to be a record for so late in the season.

On the 5 year average for the next 4 weeks, this is what I have.

+5 bcf

+21 bcf

+47 bcf

+70 bcf

Last weeks +23 bcf was compared to the 5 year average of -23 bcf.

Cash-Led Rally Sends Natural Gas Futures Higher for Second Day

5:33 PM

Natural gas futures continued to gain ground Monday despite warmer changes to weather outlooks. Strong cash prices at the end of last week that further strengthened at key pricing locations for the start of this week lent support to the futures strip, with the Nymex May contract settling 4.4 cents higher at $2.708/MMBtu and June rising 4.2 cents to $2.748.

Tuesday morning from Natural Gas Intelligence:

Natural Gas Futures Steady as Overnight Guidance Warmer, Shoulder Season Balances Loose

‘No Way’ for Natural Gas to Stay Above $3 for Long, Says Analyst

9:05 AM

Wednesday Morning NGI:

Natural Gas Futures Called Slightly Higher as More Range-Bound Action Expected

Wed night comment:

Natural Gas Futures Called Lower Ahead of EIA Report; ‘Slight Improvement’ Seen in Fundamentals

Thu am comment: 8:55 AM

Natural Gas Traders Hold Futures Positions Intact Ahead of Storage Report; Cash Mixed

Thu after report comment:

Bullish Natural Gas Storage Data No Deterrent for Bears; Permian Cash Climbs Again

EIA report just out:

+25 bcf

| Working gas in underground storage, Lower 48 states Summary text CSV JSN | |||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Historical Comparisons | |||||||||||||||||||||||||

| Stocks billion cubic feet (Bcf) | Year ago (04/05/18) | 5-year average (2014-18) | |||||||||||||||||||||||

| Region | 04/05/19 | 03/29/19 | net change | implied flow | Bcf | % change | Bcf | % change | |||||||||||||||||

| East | 209 | 210 | -1 | -1 | 219 | -4.6 | 264 | -20.8 | |||||||||||||||||

| Midwest | 240 | 241 | -1 | -1 | 249 | -3.6 | 332 | -27.7 | |||||||||||||||||

| Mountain | 64 | 64 | 0 | 0 | 84 | -23.8 | 115 | -44.3 | |||||||||||||||||

| Pacific | 119 | C | 113 | 6 | 7 | C | 170 | -30.0 | 207 | -42.5 | |||||||||||||||

| South Central | 523 | C | 502 | 21 | 23 | C | 616 | -15.1 | 722 | -27.6 | |||||||||||||||

| Salt | 166 | C | 156 | 10 | 12 | C | 195 | -14.9 | 209 | -20.6 | |||||||||||||||

| Nonsalt | 357 | 347 | 10 | 10 | 422 | -15.4 | 513 | -30.4 | |||||||||||||||||

| Total | 1,155 | C | 1,130 | 25 | 29 | C | 1,338 | -13.7 | 1,640 | -29.6 | |||||||||||||||

Friday am Natural Gas Intelligence:

Natural Gas Futures Steady; Latest Exports Data Potentially Supportive

8:52 AM

https://seekingalpha.com/article/4254210-april-2019-natural-gas-demand-overview-forecast

Summary

Natural gas consumption for January was the highest level for any month since 2001.

The average daily rate of dry natural gas production for January was the second highest for any month since EIA began tracking monthly dry natural gas production in 1973.

Under the latest weather forecasts, we project that natural gas consumption will decline in annual terms by around 1.70% (on average) over the next three months.

We have been bearish on natural gas and have been selling the rallies for the past month or so. However, we are not adding to our short exposure anymore.

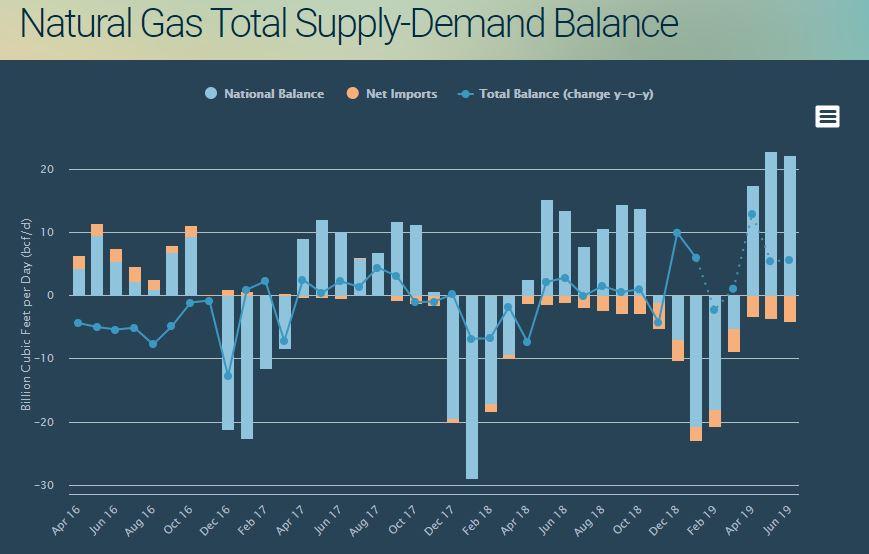

We believe that over the next three months, total supply will be growing faster (on an annualized basis) than total demand ensuring that total supply-demand balance will be looser relative to 2018.

Source: EIA, Bluegold Research estimates and calculations

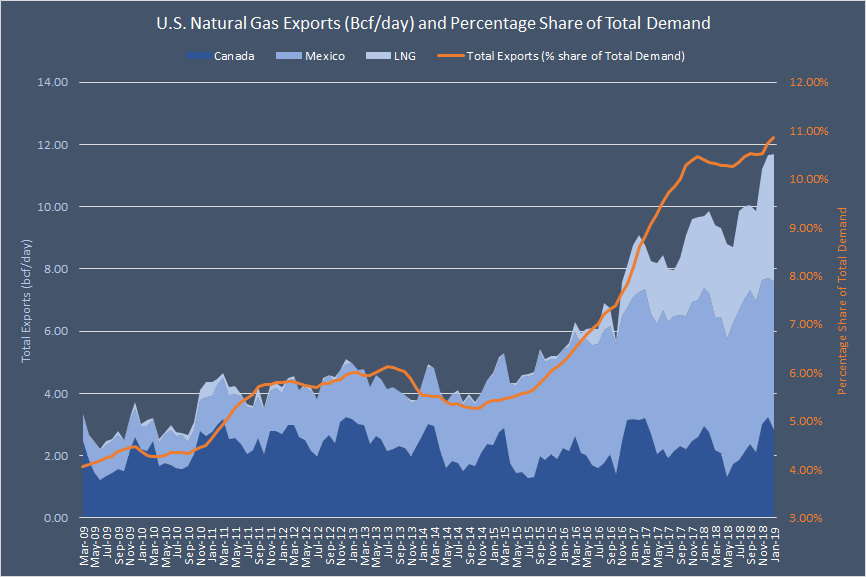

This January, pipeline and LNG exports combined totaled 362.7 bcf or 11.7 bcf per day. The volume of total exports is now equivalent to 10.7% of national natural gas consumption on a monthly basis. On a 12-month average basis, exports now equate to around 10.90% of total demand - a new all-time record - and its share in the aggregate demand structure has almost doubled over the past three years.

Exports remain the fastest-growing source of demand for American natural gas. While total demand (12-month average) increased by 20.2% over the past five years (from January 2014 to January 2019), exports more than doubled over the same period. In fact, exports have already surpassed the "Other" category in the overall demand mix and are now more significant in weight than U.S. commercial users (see the chart below). Next year, the share of exports will overtake residential consumption (on a 12-month average basis).

Source: EIA, Bluegold Research estimates and calculations