65 bcf....bearish. Even I have to admit it. Seems very bearish.

For the weather affecting residential heating demand and thus, natural gas prices, go here(much colder today) in week 2.........note, especially the overnight Canadian model ensembles analysis:

From Natural Gas Intelligence earlier:

Medium-Range Colder Trends Seen as Natural Gas Futures Surging

Storage is Very Low for this time of year!!

Storage is below the bottom of the previous 5 year range and still 580 bcf below last year at this time!

This is why the temperature forecast matters....in the Summer/cooling season and now in the early part of the key Winter/heating season............which is looking milder early on Monday.

EIA storage report on Thursday +65 bcf...........very bearish. Storage is low but supplies are gushing in. If/when it warms up, we will start eroding the big deficit.

| Working gas in underground storage, Lower 48 states Summary text CSV JSN | |||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Historical Comparisons | |||||||||||||||||||||||||

| Stocks billion cubic feet (Bcf) | Year ago (11/02/17) | 5-year average (2013-17) | |||||||||||||||||||||||

| Region | 11/02/18 | 10/26/18 | net change | implied flow | Bcf | % change | Bcf | % change | |||||||||||||||||

| East | 831 | 826 | 5 | 5 | 925 | -10.2 | 919 | -9.6 | |||||||||||||||||

| Midwest | 980 | 956 | 24 | 24 | 1,111 | -11.8 | 1,093 | -10.3 | |||||||||||||||||

| Mountain | 182 | 180 | 2 | 2 | 224 | -18.8 | 219 | -16.9 | |||||||||||||||||

| Pacific | 265 | 262 | 3 | 3 | 317 | -16.4 | 351 | -24.5 | |||||||||||||||||

| South Central | 949 | 919 | 30 | 30 | 1,210 | -21.6 | 1,246 | -23.8 | |||||||||||||||||

| Salt | 253 | 234 | 19 | 19 | 334 | -24.3 | 346 | -26.9 | |||||||||||||||||

| Nonsalt | 696 | 686 | 10 | 10 | 876 | -20.5 | 900 | -22.7 | |||||||||||||||||

| Total | 3,208 | 3,143 | 65 | 65 | 3,7 | ||||||||||||||||||||

Here's the temperature map for the 7 days going into that EIA report.

It was warmer than the previous week, so the injection WAS larger as we were expecting here.....+65bcf vs +48 bcf on the previous report.

Repeating the frigid Winter of 5 years ago, gets storage to precariously low levels and the price spikes to the highest in over a decade.

Repeating the mild Winters of 2 and 3 years ago and storage catches all the way up with last year and prices get buried into the 2's.

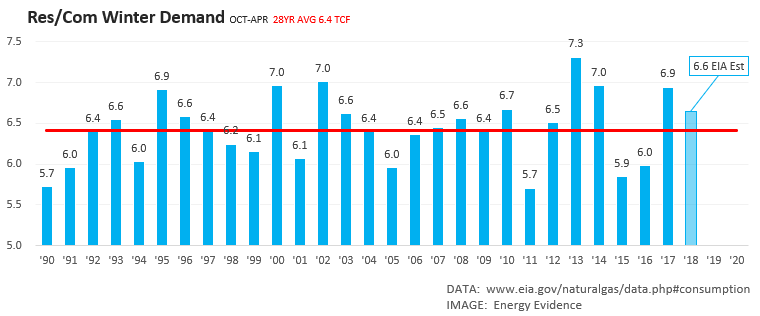

Right now EIA projects winter heating demand at about 6.6 TCF, and end of season inventories at 1.37 TCF on March 31st. Heating demand over the last 28 winters ranged from 5.7 TCF to 7.3 TCF, averaging 6.4. Here's the history from EIA:

Despite late week 2 being rather mild and the average of the last 4 CFSv2 being quite warm late week 2 and beyond, NG had a very strong day despite yesterday's bearish EIA. It is focusing on the cold week 1 through early week 2 in combination with the very low storage. It rarely focuses on the fantasyland of week 3-4, but it usually does at least partially focus on late week 2.

It does look like NG fell on the less cold 12Z Euro.

Hi Guys,

My first time posting something here. Anyway NG with a Wyckoff eye.

The objective was reached today.

http://tinypic.com/view.php?pic=2s6t15k&s=9#.W-Y5jKSWw5s

a simple student of the markets...

gedigan