AI Overview

+++++++++++++++++++++++++++++++++++++

Previous thread

VERY bad time to invest in the stock market!!

Started by metmike - June 18, 2026, 2:56 p.m.

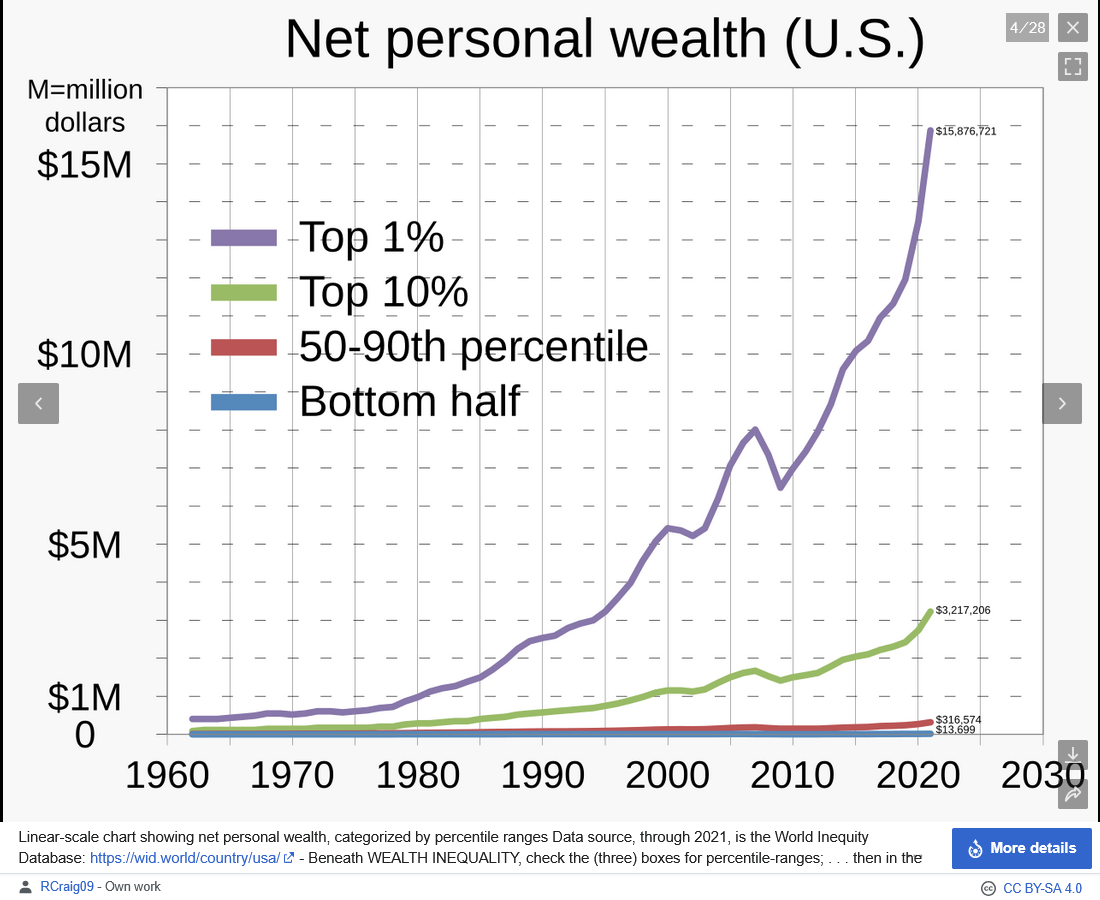

KEY TAKEAWAYS

Index-tracking funds seek to match an index’s performance, which may lead to constraints and implementation costs that hurt returns.

We find that demanding immediacy during reconstitution events leads to costs for a broad range of funds that track indices around the world.

A better approach would provide the flexibility to spread turnover across all trading days, avoiding the costs of demanding immediacy and allowing for a consistent focus on stocks with higher expected returns.

The appeal of low expense ratios and broad diversification has contributed to the growth of index funds. Yet those appealing qualities can come at a cost. Index funds primarily seek to match the performance of an index. This objective may lead to constraints and implementation costs that are not reflected in the funds’ expense ratios.

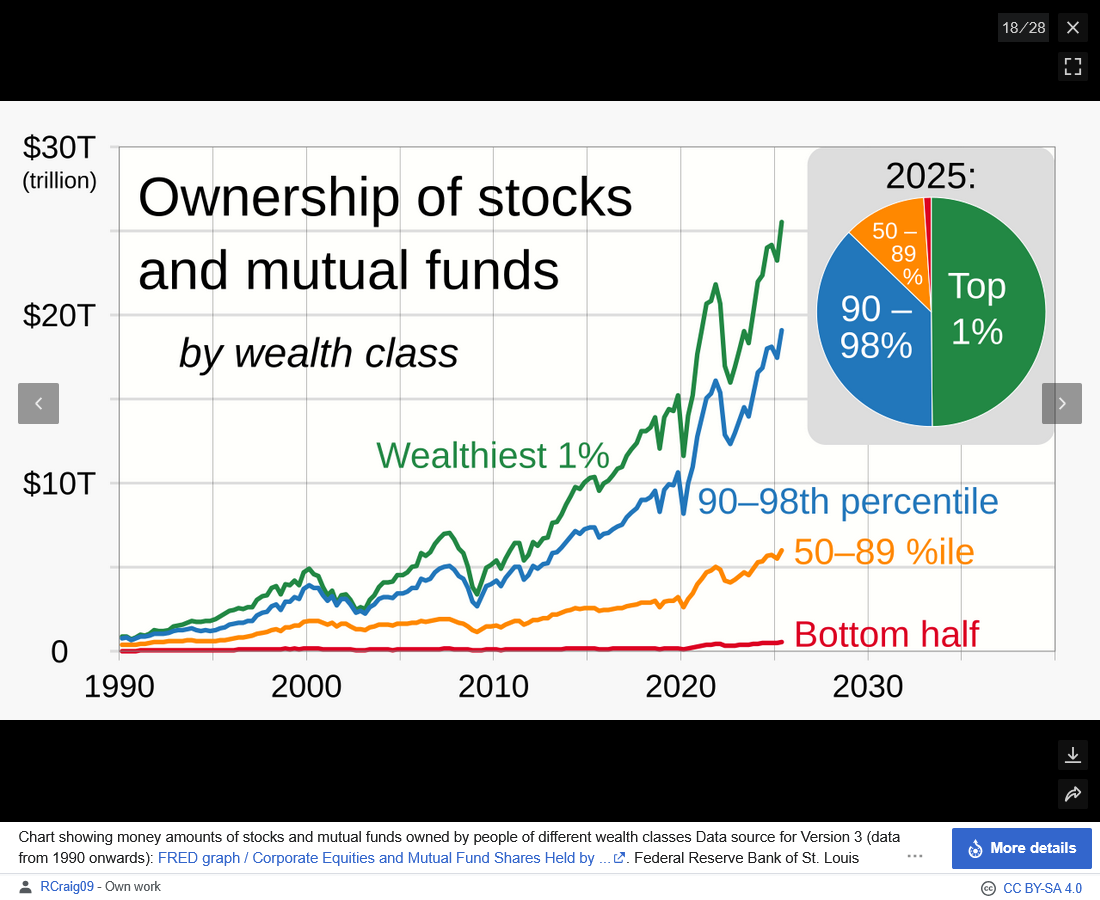

Index Funds have disrupted price discovery!

https://www.ruleoneinvesting.com/blog/investing-news-and-tips/the-looming-index-fund-bubble/

Here's the uncomfortable truth: stock prices are increasingly disconnected from business performance. A great way to see this is by looking at the Shiller PE ratio, a Nobel Prize-winning measure of market valuation.

Historically, the S&P 500 trades at around 17 times earnings. In 2025, the Shiller PE was at 38—more than double the long-term average. As of the end of January 2026, it had just gone above 40. Put another way, investors today are essentially waiting more than 38 years to get their money back from S&P 500 earnings.

Meanwhile, the market's earnings yield—the equivalent of an interest rate on stocks—is just 2.6%. Compare that with a 4.5% yield on U.S. Treasury bonds, and you can see the disconnect. Why would anyone accept less return for far more risk?

This reminds me of the late 1990s, when companies like Yahoo traded at sky-high valuations totally disconnected from reality. Back then, the bubble eventually burst. And bubbles don't deflate quietly—they pop.

Heh.

This has been pretty clear for a long time. The SPCX manipulation takes it to a France 1788 level.

Thanks, patrick,

Actually I have you to thank for this new thread.

In the conversation on the other one, I got that from reading your comments and did more investigating to better understand where you are coming from ..........and learned a ton.

And decided this is worth its own thread because it's MUCH worse than I thought I knew.

The other thread was to especially warn people about what will likely happen to the stock market during a Donald Trump impeachment.

This index fund situation has obviously been happening for many years and is independent of Donald Trump's impact, even if he is intentionally feeding it right now.

It's always a wonderful day when we learn something new and I appreciate you making yesterday so wonderful for me!

To be fair, like most things not invented by Thomas Midgley Jr., index funds serve a function and only became acutely harmful under the right conditions, and with help. From 1970 when they started, up to about 2000, just a useful way to let ordinary people share in the stock market. Throw in growing size and automated trading, and the arbitragers with super computers located near the stock market were able to bleed the market basically risk free. Still, not that big a deal, and could have been dealt with. It's only with the rise of cartoonishly evil centibillionaires, dare to be stupid, ignore fundamentals, investing and the willing collaboration of those who should be regulating, that they've become a menace.

Great way to describe it and be fair, patrick!

{kind=link}